📋 What This Guide Covers

► Quick Answer — When Rates Drop and By How Much

► The Three Stages of SR22 Rate Reduction

► Stage 1 — SR22 Removal: The First Big Drop

► Stage 2 — Violation Aging: Gradual Decline Over Years

► Stage 3 — Violation Expiration: Full Rate Recovery

► Rate Reduction Timeline by Violation Type

► Real Cost Examples — Before, During, and After SR22

► How to Speed Up Your Rate Recovery

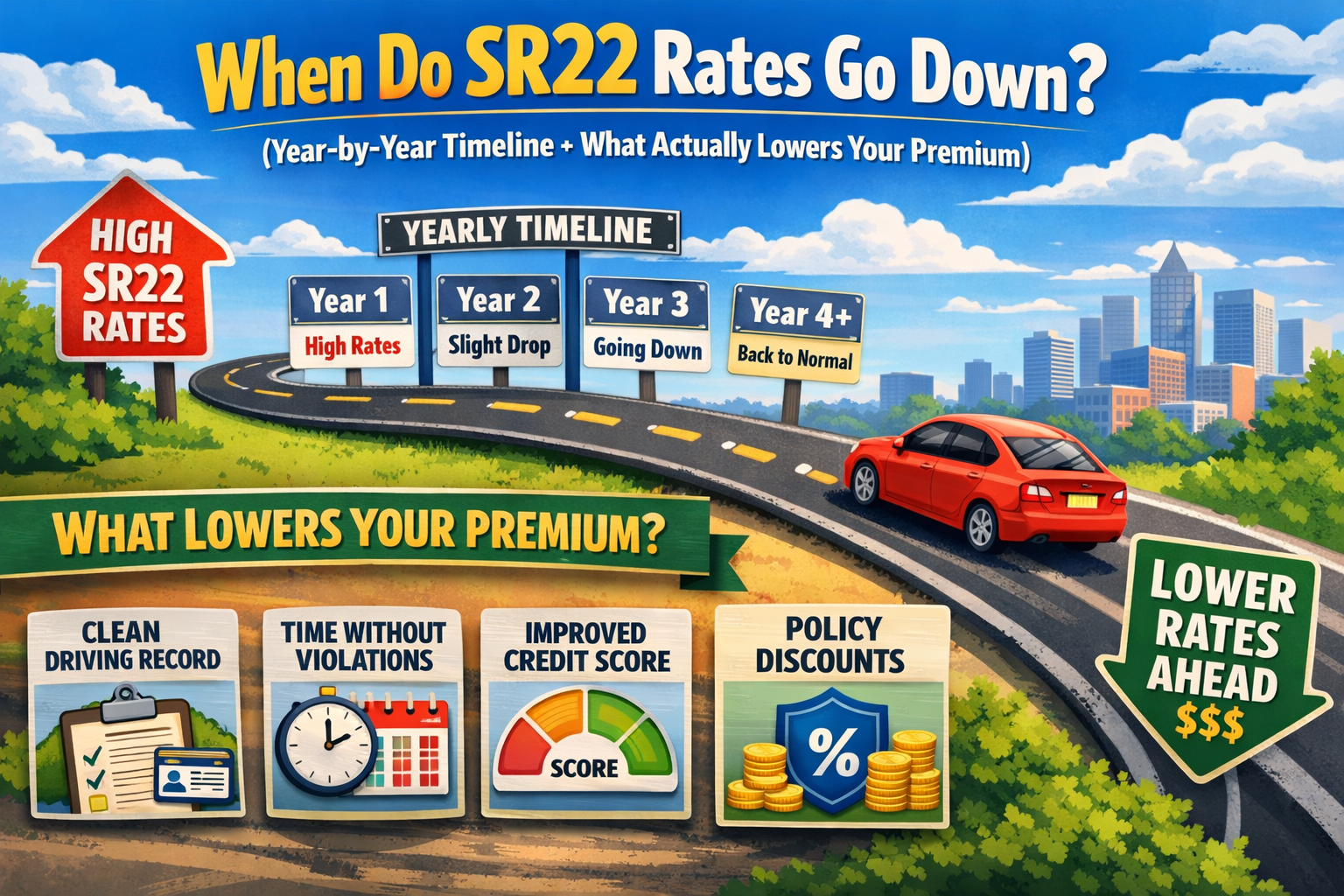

When Do SR22 Rates Go Down? — Quick Answer

The Short Answer

SR22 rates go down in three distinct stages. The first and biggest drop happens when you remove SR22 at the end of your requirement period — typically a 20 to 40 percent decrease immediately. The second stage is gradual: as your violation ages on your driving record, insurers reduce your risk classification incrementally at each annual renewal. The third and final stage happens when the violation expires off your record entirely — usually 5 to 10 years after the offense — at which point you return to near-standard rates.

The biggest mistake drivers make: not actively removing SR22 and not re-shopping after removal. Both of these inactions cost hundreds to thousands of dollars per year in premiums you no longer legally need to pay.

| Stage | When It Happens | Typical Rate Drop | Action Required |

|---|---|---|---|

| SR22 Removal | End of requirement period (typically year 2–3) | 20–40% immediate drop | You must actively request removal + re-shop |

| Violation Aging | Each annual renewal after the violation date | 5–15% per year | Re-shop annually to capture the market improvement |

| Violation Expiration | 5–10 years after offense (varies by state and violation) | Return to near-standard rates | Re-shop immediately when violation drops off record |

The key insight most drivers miss: none of these rate reductions happen automatically unless you take action. SR22 is not removed automatically when the requirement ends — you must request it. And even if SR22 is removed, your current insurer has no incentive to proactively lower your rate. Re-shopping after every stage is the only way to fully capture each rate reduction as it becomes available.

The sections below give you the complete, year-by-year timeline for your specific violation type, real dollar amounts, and every strategy available to you. For the full SR22 overview including all costs and the filing process, see our ultimate guide to SR22 insurance.

The Three Stages of SR22 Rate Reduction — How the System Works

Understanding why rates drop — and when — requires understanding how insurance companies actually price high-risk drivers. SR22 insurance is expensive for a specific reason: you have been flagged by your insurer as a statistically elevated risk based on one or more serious violations. That elevated risk classification drives your premium up, and it only comes down as the indicators of elevated risk diminish over time.

Insurers look at two separate but related signals when pricing a high-risk driver. The first signal is whether SR22 is currently required — meaning the government has independently determined you are a threat to public safety and imposed an active monitoring requirement. The second signal is the underlying violation on your driving record — the DUI, reckless driving charge, or series of violations that triggered the requirement in the first place. Both signals affect your premium. And both decline on different timelines.

Why SR22 Removal Causes a Rate Drop

When SR22 is active on your record, insurers apply what is effectively a compliance surcharge on top of the violation surcharge. Having an active SR22 requirement is a real-time signal to every insurer that the government currently considers you a high-risk driver requiring state monitoring. When SR22 is removed, that active monitoring flag disappears from your record. Insurers can see that the requirement has ended, which signals you have successfully completed the required high-risk compliance period. This removal alone produces a meaningful rate reduction at your next renewal — even though the underlying violation is still on your record.

Why Violations Age and Become Less Impactful Over Time

Insurance pricing is based on statistical risk prediction. A DUI from three years ago is a worse risk indicator than one from seven years ago — because seven years of subsequent clean driving demonstrates that the behavior was either situational or has been corrected. Insurers quantify this mathematically: the risk weight assigned to any violation decreases as time passes without recurrence. At every annual renewal, the same violation is slightly older, slightly less predictive of future claims, and therefore priced slightly lower.

This gradual aging process produces incremental rate decreases at each annual renewal — typically 5 to 15 percent per year, compounding over time. A driver who was paying $310 per month at the start of their SR22 period might be paying $230 per month three years later and $145 per month six years after the violation — even though the violation is still technically on their record. The trajectory is steady and meaningful.

Why Violation Expiration Produces the Final Full Recovery

Every state sets a look-back window for driving violations — the period during which the violation is legally visible on your record for insurance pricing purposes. When a violation reaches the end of that window, it expires off the record entirely. Insurers who pull your Motor Vehicle Report (MVR) after expiration literally cannot see the violation anymore. It is gone from the pricing calculation. At that point, insurers price you based only on your current record — and if that record has been clean throughout the SR22 period and beyond, you qualify for standard or near-standard rates.

The look-back window varies by state and violation type: most states retain minor violations for 3 to 5 years; DUI and serious violations are retained for 5 to 10 years; California retains DUI for 10 years. Full expiration timelines by state and violation type are in the sections below.

Stage 1 — SR22 Removal: The First Big Rate Drop

The single most impactful thing you can do to reduce your insurance rate is remove SR22 the moment your requirement ends. The rate drop at SR22 removal is the largest single pricing decrease you will see — typically 20 to 40 percent off your current premium — and it happens within the first renewal cycle after removal.

How Much Rates Drop at SR22 Removal

The rate reduction at SR22 removal is not uniform — it depends on your violation type, state, age, and which insurer you use. The following table shows typical monthly premium ranges during active SR22 versus after removal (but while violation still on record) for minimum liability coverage in a mid-cost state.

| Violation | During Active SR22 | After SR22 Removal | Immediate Savings |

|---|---|---|---|

| First DUI | $220–$390/mo | $145–$265/mo | $75–$125/mo savings |

| Reckless Driving | $128–$390/mo | $92–$255/mo | $36–$135/mo savings |

| Driving Without Insurance | $88–$210/mo | $72–$155/mo | $16–$55/mo savings |

| Multiple Violations (points) | $105–$240/mo | $82–$178/mo | $23–$62/mo savings |

| FR44 (FL/VA DUI) | $265–$505/mo | $175–$350/mo | $90–$155/mo savings |

Why SR22 Removal Does NOT Happen Automatically

This is the most expensive passive mistake in all of SR22. When your requirement period ends, your policy continues exactly as it is — with the SR22 endorsement active, the associated compliance flag on your record, and the elevated premium — until you take explicit action to remove it. Your insurer has no legal obligation and no financial incentive to notify you that your SR22 requirement has ended. Many drivers continue paying full SR22-level premiums for 6, 12, or even 24 months after their requirement ended simply because no one told them they needed to act.

A DUI driver paying $280 per month who should have removed SR22 12 months ago has overpaid by approximately $1,200 to $1,800 depending on their state and insurer — assuming they would have found a $180 post-removal rate after re-shopping. This money is simply lost. It does not come back. The only defense is active calendar management.

Exactly How to Remove SR22 and Capture the Rate Drop

Step 1: Call your state DMV and get your official SR22 end date in writing. Do not calculate this yourself — the clock started at suspension, lapses may have extended it, and your estimate may be wrong. Get the confirmed date from the DMV directly.

Step 2: Set a calendar reminder 60 days before that end date. Use this window to start shopping for new insurance rates — because you will want to re-shop immediately upon removal, and having quotes ready means you capture the savings on day one rather than months later.

Step 3: On or after your official end date (never before — requesting removal early creates a lapse), call your insurer and say: “My SR22 requirement has ended as of [date]. I need you to file the SR26 completion notice with the DMV and remove the SR22 endorsement from my policy.” Get written confirmation that this has been done.

Step 4: Re-shop immediately. Your current insurer will apply a modest rate reduction at your next renewal. But that reduction is almost certainly smaller than the competitive rate you can find by shopping among insurers who now see you as a post-SR22 driver rather than an active high-risk filing. The re-shopping step is where the real money is. Full details in our SR22 removal guide.

Why You Must Re-Shop — Not Just Remove

Staying with your SR22 insurer after removal almost always costs more than switching. SR22 specialty insurers — Dairyland, Bristol West, The General — charge premiums structured around high-risk driver risk pools. When you remove SR22, you are no longer required to be in their risk pool, but you remain there by default. Standard and near-standard insurers like GEICO, Progressive, and Nationwide will now quote you at much lower rates. The typical gap between your SR22 insurer’s post-removal rate and the best available market rate is $40 to $120 per month — $480 to $1,440 per year that loyalty to your old insurer costs you unnecessarily.

Stage 2 — Violation Aging: The Gradual Annual Decline

Between SR22 removal and full violation expiration — which can be 2 to 7 years apart — your rates do not sit still. Each year that passes without a new violation moves the existing offense further into your past, reduces its statistical weight as a risk predictor, and produces modest rate reductions at each annual renewal. This compounding, year-over-year improvement is significant in total even if each individual step is small.

How Much Rates Decline Each Year After SR22 Removal

The year-over-year decline depends heavily on violation type. DUI is weighted more heavily than most other violations and maintains a larger surcharge for longer. No-insurance violations fade faster. The table below shows a representative rate trajectory for a first DUI driver in a mid-cost state, starting from the point of SR22 removal.

| Years Since DUI | Status | Est. Monthly Rate | vs. Peak SR22 Rate |

|---|---|---|---|

| Year 0–1 | Active SR22 (peak) | $290–$350/mo | Baseline high |

| Year 3 (SR22 removed) | Post-removal, violation still on record | $190–$240/mo | ~30% lower |

| Year 4 | Aging, violation still on record | $168–$215/mo | ~40% lower |

| Year 5 | Aging, violation still on record | $148–$192/mo | ~46% lower |

| Year 7 | Aging, most states violation near expiry | $118–$158/mo | ~55% lower |

| Year 10 (CA DUI expires) | Violation fully off record | $82–$115/mo | ~70–75% lower — near standard |

Why Re-Shopping Every Year Is Essential During This Stage

The gradual rate reduction from violation aging does not appear automatically with your current insurer. Here is why: your current insurer re-evaluates your risk profile at each annual renewal. They will reduce your premium modestly as the violation ages. But their reduction is based on their own actuarial models and their own internal risk classification — not on the full competitive market.

Other insurers in the market are also re-pricing drivers with aging violations — and their models may produce materially different (lower) rates than your current insurer’s annual renewal price. A driver who has had a clean 18-month post-SR22 record may find that a competitor is now willing to quote them at $138 per month while their current insurer is only down to $172. The $34 monthly difference — $408 per year — is available only through comparison shopping. It does not come to you; you have to go get it.

The rule: re-shop your insurance every 12 months without exception during the period between SR22 removal and full violation expiration. Every renewal cycle is an opportunity to capture market-level pricing for your current risk profile. Set a calendar reminder 30 days before each renewal date. See our cheapest SR22 companies guide for who is most competitive at each post-violation stage.

What Slows Down the Aging Process — Avoiding New Violations

The aging benefit only accumulates if you maintain a clean record. Any new violation during this period resets the risk clock. A new speeding ticket at year 4 post-DUI adds a fresh violation surcharge on top of the aging DUI surcharge — slowing or reversing the downward rate trajectory. A second DUI at year 4 would be catastrophic: new SR22 requirement, dramatically higher premiums, potential for extended look-back windows, and the original DUI’s aging progress lost to the combined risk of two serious violations in a relatively short period.

Every year of clean driving is worth real money in premium reduction. Every new violation is a premium increase that compounds on top of existing surcharges. The financial incentive to drive carefully during the post-SR22 period is not abstract — it is measured in hundreds of dollars per year in insurance savings.

Stage 3 — Violation Expiration: Full Rate Recovery

The final stage of rate recovery happens when your violation expires off your driving record entirely. At this point, insurers who pull your Motor Vehicle Report (MVR) no longer see the violation — it is gone from their pricing inputs. If your record has been clean throughout the SR22 period and beyond, you now present as a driver with no significant violations, and insurers price you accordingly. This is when rates return to near-standard levels.

How close to standard depends on the rest of your profile: your age, credit score (in applicable states), the specific insurer, and whether any minor violations remain on your record. Drivers who maintain completely clean records after SR22 and have good credit often achieve rates within 10 to 15 percent of the best available standard rates — effectively returning to normal after what was a 5 to 10 year elevated rate period.

How Long Violations Stay on Your Record — By State and Violation Type

| Violation | Most States | California | Florida | Texas |

|---|---|---|---|---|

| First DUI / DWI | 5–7 years | 10 years | 10 years | 10 years |

| Second DUI | 7–10 years | 10 years | Permanent | 10 years |

| Reckless Driving | 3–5 years | 7 years | 5 years | 3 years |

| Driving Without Insurance | 3 years | 3 years | 3 years | 3 years |

| Speeding (minor) | 3 years | 3 years | 3 years | 3 years |

| At-Fault Accident | 3–5 years | 3 years | 3 years | 3 years |

Note: These are insurance look-back periods, which may differ from the criminal record retention period. Always confirm your specific state’s current rules as these windows can change with legislation.

What to Do When Your Violation Expires

Violation expiration — like SR22 removal — is not a passive event that automatically produces better rates. Your current insurer may not proactively pull a new MVR at renewal. They may continue pricing you based on the last MVR they pulled — which still showed the violation. To fully capture the benefit of violation expiration, you need to actively re-shop with multiple insurers and explicitly tell them to pull a fresh MVR.

Keep a note of your violation date. Calculate when it expires in your state using the table above. Set a calendar reminder 60 days before expiration. When that date arrives, get quotes from 5 or more insurers with a current MVR pull. The rate difference between a quote pulled while the violation is still visible and a quote pulled after it has expired can be $50 to $150 per month — a difference that shows up immediately in your first renewal quote post-expiration.

Rate Reduction Timeline by Violation Type

Different violations follow different rate recovery timelines. Here is what to expect for each major SR22-triggering offense.

First DUI — The Longest Road to Recovery

A first DUI produces the most dramatic premium increase and has the longest recovery trajectory. The full timeline in a 3-year SR22 state with 7-year record retention looks like this:

Year 0–3 (Active SR22): Peak premiums, 150 to 300 percent above standard. No meaningful rate relief during this window. Lapse prevention is the only cost control strategy that matters.

Year 3 (SR22 removed): 20 to 40 percent drop immediately upon removal and re-shopping. This is the biggest single improvement in the entire timeline. Do not delay acting on this.

Years 4–6 (Post-removal aging): 8 to 15 percent additional annual improvement as the violation becomes older. Re-shopping every renewal is essential to capture competitive market rates at each stage.

Year 7 (DUI expires in most states): Major additional drop as the violation disappears from MVR. Driver can now be priced as standard or near-standard if remaining record is clean. Final re-shop required to fully capture this.

Year 10 (DUI expires in California, Florida, Texas): Final and full rate recovery available. A California DUI driver who was paying $350 per month at peak might reach $88 to $110 per month after clean 10-year record. Total premium paid over the full 10-year period from DUI to full recovery: $15,000 to $32,000 depending on state, age, and insurer decisions. For the full DUI cost analysis see our SR22 after DUI guide.

Driving Without Insurance — Faster Recovery

Year 0–3 (Active SR22): Premiums 30 to 80 percent above standard. More insurer options than DUI — non-specialist insurers will sometimes write these policies.

Year 3 (SR22 removed): 15 to 30 percent drop upon removal. More modest than DUI because the starting premium was lower.

Years 3–5 (Post-removal aging): Gradual 5 to 10 percent annual improvement.

Year 5–6 (Violation expires in most states): Near full recovery to standard rates. Total elevated premium period is typically 5 to 6 years for a first no-insurance offense — shorter than DUI and with lower peak costs.

Reckless Driving — Mid-Range Recovery

Year 0–3 (Active SR22): Premiums 80 to 180 percent above standard. Wet reckless (DUI plea bargained down) is priced at the higher end of this range by many insurers.

Year 3 (SR22 removed): 20 to 35 percent drop upon removal.

Years 3–7 (Aging and expiration): Steady recovery toward standard rates as the 3 to 7-year look-back window passes. Wet reckless may stay on record as long as standard reckless in most states — confirm your specific state’s handling.

Multiple Violations / Points Suspension — Depends on Individual Tickets

A points-based SR22 requirement typically results from multiple minor violations — speeding tickets, failure to yield, improper lane changes. Each individual ticket has its own 3-year look-back window. The rate recovery timeline depends on when each ticket expires. A driver with three tickets over 24 months faces a 3-year elevated rate period for the last ticket, after which rates return to near-standard relatively quickly — because no single ticket carries the weight of DUI. The peak surcharge is lower (25 to 70 percent above standard), recovery is faster, and the total elevated-rate period is shorter. The strategy is identical: remove SR22 at requirement end, re-shop at every renewal, and re-shop when the last ticket expires.

Rate Recovery by State — Key Differences

Your state significantly affects both how fast your rates recover and how much you ultimately save. State-level variables include the SR22 duration itself (which determines how long you are at peak rates), the violation look-back window (which determines total elevated rate duration), baseline insurance costs (which affect the raw dollar magnitude of changes), and whether credit can be used in pricing (which affects available rate improvement strategies).

| State | SR22 Duration (DUI) | DUI Record Retention | First Big Drop | Full Recovery |

|---|---|---|---|---|

| California | 3 years | 10 years | Year 3 (removal) | Year 10 |

| Texas | 2 years | 10 years | Year 2 (removal) | Year 10 |

| Florida (FR44) | 3 years | 10 years | Year 3 (removal) | Year 10 |

| Illinois | 3 years | 5 years | Year 3 (removal) | Year 5–6 |

| Georgia | 3 years | 5 years | Year 3 (removal) | Year 5–6 |

| Ohio | 3 years | 6 years | Year 3 (removal) | Year 6–7 |

California — The Most Difficult Rate Recovery

California DUI drivers face the longest rate recovery in the country. The 10-year record retention window — longest of any state — means the DUI remains visible to every insurer for a decade. Combined with some of the highest base insurance costs in the country and the clock-reset lapse policy that can extend the SR22 period beyond 3 years, California DUI total cost is consistently the highest nationally. A California driver with a 2026 DUI who successfully removes SR22 in 2029 still has the DUI affecting their insurance rates until 2036. Total premium impact over that decade: $18,000 to $40,000 depending on age and insurer choices.

Note that California prohibits the use of credit in insurance pricing. Improving your credit score — a viable cost-reduction strategy in 46 other states — does not help in California. The available strategies are limited to quote comparison, defensive driving discounts, and clean record accumulation.

Texas — Earlier First Drop, Still Long Full Recovery

Texas’s 2-year SR22 duration means the first major rate drop comes at year 2 rather than year 3 — a full 12 months earlier than most states. This is meaningful: at $218 to $398 per month, saving one year of SR22 premium means $2,616 to $4,776 in avoided peak-rate costs. However, the 10-year DUI record retention means Texas mirrors California on total recovery timeline. The earlier first drop makes Texas one of the more financially manageable DUI states despite the long retention window.

Illinois and Georgia — Shorter Record Retention, Faster Full Recovery

With 5-year DUI record retention in both states, drivers in Illinois and Georgia achieve full rate recovery about 5 years faster than California or Texas drivers with the same violation. The first major drop still comes at year 3 (SR22 removal), but the remaining elevated rate period is only 2 to 3 years rather than 7 years. A Georgia DUI driver who manages the process well — removes SR22 promptly, re-shops at every renewal, maintains a clean record — may return to near-standard rates within 5 to 6 years of the offense. This makes the total elevated premium period significantly shorter and less expensive than in high-retention states.

Real Cost Examples — Before, During, and After SR22

The following examples show the complete rate trajectory for real-profile drivers — from pre-violation standard rates through peak SR22 period, post-removal aging, and eventual full recovery. All examples assume the driver shops competitively at each stage and removes SR22 promptly at the end of the requirement period.

Example 1 — Georgia First DUI, Age 34, Competitive Shopper

| Period | Monthly Rate | Annual Cost |

|---|---|---|

| Pre-DUI (standard) | $88 | $1,056 |

| Year 0–3 (Active SR22) | $235 | $2,820 |

| Year 3–4 (Post-removal, violation on record) | $158 | $1,896 |

| Year 4–5 (Aging) | $138 | $1,656 |

| Year 5–6 (Violation expires in GA) | $95 | $1,140 |

| Total premium over 6 years (elevated period) | — | $10,980 (vs. $6,336 at standard) |

By competitive shopping at every stage and removing SR22 promptly, this driver saved an estimated $3,200 vs. staying with the original insurer throughout. Without re-shopping, year 3 rate would have been ~$195 instead of $158, costing an extra $444/year.

Example 2 — Texas First DWI, Age 28, Re-Shops Every Renewal

| Period | Monthly Rate | Annual Cost |

|---|---|---|

| Pre-DWI (standard) | $95 | $1,140 |

| Year 0–2 (Active SR22) | $218 | $2,616 |

| Year 2–4 (Post-removal) | $148 | $1,776 |

| Year 4–7 (Aging) | $125–$108 | ~$1,392 |

| Year 10+ (DWI expires in TX) | $98 | $1,176 |

| Texas 2-year SR22 advantage vs 3-year state | — | ~$2,616 saved vs extra year of SR22 |

Example 3 — Ohio No-Insurance Violation, Age 34 — Fastest Recovery

| Period | Monthly Rate | Annual Cost |

|---|---|---|

| Pre-violation (standard) | $72 | $864 |

| Year 0–3 (Active SR22) | $120 | $1,440 |

| Year 3–5 (Post-removal aging) | $92–$80 | ~$1,032 |

| Year 5+ (Violation off record) | $74 | $888 — near full recovery in 5 years |

How to Speed Up Your SR22 Rate Recovery

You cannot change your violation date or remove it from your record early. But you have significant control over how much you pay at every stage of the recovery timeline. These strategies produce real, measurable premium reductions throughout the SR22 period and after.

1. Maintain an Absolutely Clean Record Going Forward

The single most impactful thing you can do to accelerate rate recovery is to not add any new violations. Every new ticket or at-fault accident adds a fresh surcharge on top of the existing one, extending the elevated rate period and slowing the aging process. A driver with one aging DUI from 4 years ago plus a new speeding ticket is priced significantly worse than a driver with only the 4-year-old DUI. The math is straightforward: the rate reduction from 4 years of clean driving following a DUI is often $80 to $130 per month. A new speeding ticket at year 4 can add $40 to $80 per month — eliminating half or more of the aging benefit gained. Drive carefully. Use adaptive cruise control and navigation apps for speed alerts. The financial stakes of a traffic violation are much higher for you during this period than they are for a driver with a clean record.

2. Improve Your Credit Score (In 46 States)

Credit-based insurance scoring is used by insurers in 46 states (not California, Hawaii, Massachusetts, or Michigan). The relationship between credit and insurance rates is statistically significant: a driver with a 580 credit score typically pays 20 to 35 percent more than a driver with the same violations and a 720 credit score. During a 3-year SR22 period, improving your credit score from the 580 range to 680 can reduce your monthly premium by $30 to $80 — savings of $1,080 to $2,880 over 36 months on top of any other improvements.

Credit improvement during an SR22 period is achievable because the timeline aligns: improving credit from poor to fair typically takes 12 to 24 months of consistent positive activity. If you start credit improvement at the beginning of your SR22 period, you may have meaningfully improved credit by the time you are mid-period — at which point a re-quote will capture the combined benefit of aging violation and improved credit. Credit improvement strategies: pay all existing accounts on time, pay down revolving balances below 30 percent utilization, avoid new hard inquiries, and dispute any incorrect items on your credit report.

3. Complete a Defensive Driving Course

Many states allow a state-approved defensive driving course to remove points from your record or qualify for insurance premium discounts of 5 to 10 percent. Not all insurers honor this discount for SR22 drivers — confirm directly with your insurer before enrolling. For drivers whose SR22 was triggered by points accumulation rather than DUI, a defensive driving course may also reduce the point total on your record, which can meaningfully affect how insurers price your risk during the aging period. Cost of a state-approved defensive driving course: typically $30 to $100. Annual savings if the discount applies: $180 to $420 on a $3,000/year policy.

4. Switch to a Non-Owner Policy If Your Vehicle Situation Changes

If at any point during your SR22 period you sell your vehicle and do not replace it immediately, switching to a non-owner SR22 policy can save $100 to $295 per month. Non-owner policies are priced significantly lower than owner policies because they cover infrequent use of non-owned vehicles. Drivers who move to a city with strong public transit, need only occasional use of a family member’s car, or are temporarily without a vehicle should confirm with their insurer whether a non-owner policy switch is appropriate for their situation. Full details in our non-owner SR22 guide.

5. Pay Annually Rather Than Monthly

Most insurers offer a 5 to 10 percent discount for paying the full annual premium upfront. On a $240 per month policy, a 7 percent annual discount saves $202 per year — $606 over the 3-year SR22 period. The savings compound: if you also improve your credit and find a cheaper insurer at year 1, paying annually at the lower rate saves even more. This discount requires access to the lump sum at renewal, but for drivers who can manage it, the return is consistent and predictable.

6. Never Allow a Coverage Lapse

A coverage lapse during the SR22 period is the most expensive event that can happen to your rate trajectory. Beyond the direct consequences — license re-suspension, reinstatement fees, potential clock reset — a documented lapse results in 40 to 60 percent higher premiums when you re-insure compared to what you would have paid without the lapse. A driver who was paying $235 per month and lapses pays $329 to $376 when they restore coverage. That additional $94 to $141 per month persists for 12 to 24 months before it begins to moderate. Total lapse premium penalty over 18 months: $1,692 to $2,538. Set autopay on day one and treat it as non-negotiable. Details on preventing lapses are in our SR22 lapse consequences guide.

When and How to Re-Shop After SR22 — The Exact Playbook

Re-shopping insurance is not complicated. Most drivers avoid it out of inertia — it feels like a hassle and they assume the savings won’t be worth the time. This is the most expensive passive mistake post-SR22 drivers make. A 30-minute comparison shopping session at each renewal can save $500 to $1,500 per year. Here is the exact playbook, by trigger event.

Re-Shop Trigger #1 — Immediately After SR22 Removal

This is the highest-value re-shop moment in the entire post-SR22 timeline. When SR22 is removed from your record, you shift from a pool of active high-risk drivers to a pool of post-violation drivers — and the insurers who compete for these two pools are different. Your current SR22 specialist insurer will apply some rate reduction. But standard insurers — who may have been unwilling to quote you at all while SR22 was active — now see you as a competitive prospect.

Who to contact: Go beyond your current insurer and the SR22 specialists. Add GEICO, Progressive (if not your current), Nationwide, Travelers, and local or regional insurers to your quote list. Post-SR22 removal, these standard insurers often produce the most competitive quotes for a driver with a clean post-violation record and improving credit.

What to tell each insurer: “I recently had an SR22 requirement removed — my coverage requirement ended on [date]. My record since the original violation has been completely clean. I need current rate quotes for minimum liability coverage.” Always mention that your record post-violation is clean — this is a meaningful positive signal that insurers weight positively.

Re-Shop Trigger #2 — Every Annual Renewal

After SR22 removal, re-shop your insurance at every annual renewal for as long as the violation remains on your record. The insurance market for post-violation drivers is dynamic: insurers’ willingness to compete for your business — and the rates they offer — changes year over year as the violation ages. A insurer that was unwilling to compete for a 2-year-old DUI may actively price to win your business at year 4.

Practical approach: Set a calendar reminder 30 days before your renewal date. Get quotes from at least 5 insurers. If your current insurer’s renewal quote is not within $20 per month of the best alternative, switch. The friction of switching is low — it takes one phone call. The savings from not switching can be $500 to $1,200 per year.

Re-Shop Trigger #3 — When Your Violation Expires

Mark the violation expiration date in your calendar. When it arrives, this is the final and largest re-shop opportunity of the entire post-SR22 recovery timeline. With the violation gone from your MVR, you are now eligible to be quoted as a near-clean driver. Standard insurers will compete aggressively for your business.

What to do: Get quotes immediately from a broad range of insurers — including major standard carriers you have not been able to use for years. Tell each insurer: “I had a [violation type] from [year] that has now expired off my record. My record since that time has been completely clean. Please pull a current MVR and quote me based on my current record.” Having the insurer pull a current MVR ensures they see the expiration — some insurers retain internal records of violations longer than the state reporting window and may price based on that internal history unless explicitly asked to quote based on current MVR.

✓ Complete Post-SR22 Re-Shopping Calendar

■ 60 days before SR22 end date: Begin gathering quotes from both SR22 specialists and standard insurers

■ Day of SR22 removal: Request removal from insurer, confirm DMV processing, immediately compare new quotes

■ Every renewal date after removal: Get 5+ quotes 30 days before renewal. Switch if savings exceed $20/mo

■ 1 year post-removal: Re-quote — insurers often become newly competitive after 12 months of clean record post-SR22

■ 60 days before violation expiration: Begin gathering quotes, ask each to pull fresh MVR at expiration

■ Day violation expires: Get 5+ quotes from full market including standard carriers, switch to best rate

For current rate data and which insurers are most competitive at each stage of post-SR22 recovery, see our cheapest SR22 companies guide and the full ultimate SR22 guide.

Frequently Asked Questions

How much do SR22 rates go down after the requirement ends?

SR22 rates typically drop 20 to 40 percent when the requirement is removed and you re-shop with competitive insurers. The exact amount depends on violation type, state, age, and how aggressively you shop. A DUI driver paying $280 per month during SR22 might find rates of $165 to $200 per month after removal — a savings of $80 to $115 per month. This reduction is only captured by actively removing SR22 and re-shopping. Neither happens automatically.

Do SR22 rates go down while SR22 is still active?

Modestly. During the active SR22 period, the violation surcharge remains essentially full size — the government monitoring requirement is still active, signaling ongoing elevated risk. Your rates may decrease slightly year-over-year as the violation ages, but the reduction while SR22 is active is minor compared to the drop at removal. The most effective action during active SR22 is re-quoting at each annual renewal to ensure you are at the competitive market rate among SR22 insurers — not to find meaningful rate reductions, but to avoid overpaying.

Will insurance rates ever fully return to normal after a DUI?

Yes — but it takes years. In most states with 5 to 7-year DUI record retention, a driver who maintains a completely clean record and good credit for the full period returns to near-standard rates after the violation expires. The recovery is not to exactly the pre-DUI rate — other factors like age, vehicle, and the specific insurer affect final pricing — but the DUI surcharge is fully eliminated once the violation is no longer visible on the MVR. In California, Florida, and Texas with 10-year retention, full recovery takes a decade. In Illinois and Georgia with 5-year retention, full recovery may come in 5 to 6 years from the original offense.

My SR22 ended 2 months ago — why is my rate still the same?

Two things may have happened. First, if SR22 is still showing on your DMV record — because you have not yet requested removal from your insurer — your insurer still sees an active SR22 requirement and prices accordingly. Request removal immediately. Second, if you requested removal but stayed with the same insurer, their rate adjustment happens at your next annual renewal — not immediately. Re-shopping now with multiple insurers will capture the current market rate for a post-SR22 driver, which is almost certainly lower than what your current insurer will offer at renewal.

How long does SR22 stay on your driving record?

The SR22 notation itself — the active requirement flag — is removed from your record when you file for removal after the requirement ends. This typically happens within 1 to 2 business days of your insurer filing the SR26 completion notice. The underlying violation that triggered SR22 remains on your record separately, on the state-specific look-back window timeline: 3 to 5 years for most non-DUI violations, 5 to 10 years for DUI depending on state.

Can a new speeding ticket undo my SR22 rate progress?

Yes, significantly. A new speeding ticket during or after your SR22 period adds a fresh violation surcharge on top of whatever aging benefit you have accumulated. Depending on the ticket severity, this can add $25 to $75 per month — partially or fully eliminating the rate reduction you had gained. If the new violation is serious enough (reckless driving, second DUI), it can restart an SR22 requirement entirely. Every traffic citation during the recovery period is financially costly beyond just the fine — the insurance surcharge is almost always the larger cost.

Does improving my credit during SR22 help my rates right away?

Not immediately — credit-based insurance scoring is typically applied at policy renewal, not mid-term. When you re-shop at renewal, insurers pull a new credit check and apply the updated score to their pricing. If your credit has improved since you last shopped, the improvement will show up in new quotes. This is why starting credit improvement early in the SR22 period — even if the benefit doesn’t appear immediately — produces meaningful savings by the time your first or second renewal arrives.

Is it worth switching insurers to save $30 per month after SR22?

Yes. $30 per month is $360 per year. Switching insurers takes approximately one hour of work — one phone call to your current insurer and one to the new insurer. That works out to roughly $360 in savings per hour of effort. No other activity produces a comparable return. The concern about losing loyalty discounts or continuity is largely unfounded — any loyalty discount your current insurer offers is already baked into their renewal quote. If the best market quote is $30 lower, that gap exists even after loyalty pricing. Switch.

How do I know when my violation will expire off my record?

Add the state’s look-back window to the date of your violation. For a DUI in Illinois (5-year window) that occurred on March 15, 2022, the violation expires for insurance purposes around March 15, 2027. You can confirm your specific state’s look-back period by contacting your state DMV or Department of Insurance, or by reviewing your state’s motor vehicle code. Mark the expiration date in your calendar and schedule a comprehensive insurance re-shop starting 60 days before that date.